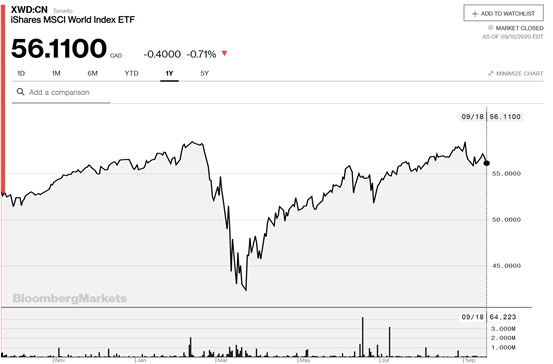

In March 2020, the MSCI World index crashed 28% as pandemic anxiety weighed down on the market. By the end of Q3 2020, it had climbed back to a previous peak and then made a 4% correction from the most recent peak in September. How do you invest smartly and safely to ensure you are not caught in such volatile times?

1. Reduce Risks, Diversify

Trying to time the market – that is, to move in and out of a financial market by attempting to predict future price movements – is not recommended, There are too many unknown variables all the time.

Don’t put all your eggs in one basket, but some baskets are better than others at certain times – these are the baskets we want to be in.

Diversify by including safer investments in your portfolio. Diversification can help in risk mitigation; you can safeguard yourself better against adverse market cycles, get access to more opportunities, and soften the impact of volatility. For example, look at how indices such as the S&P 500 have grown consistently over 10- to 15-year timeframe. As such, the likelihoods of netting returns on lower-risk investments are exponentially higher over the long run.

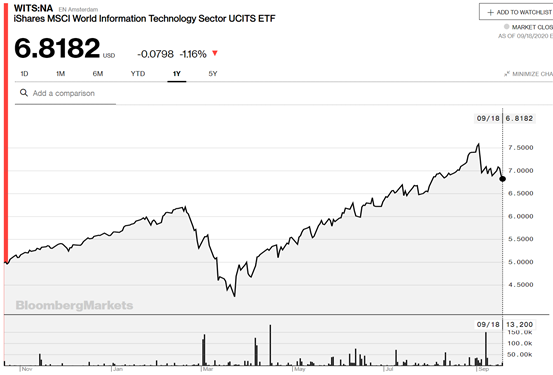

Tech stocks, for instance, have gained 78% by early September 2020 from rock bottom in March, whereas MSCI World gained only 38%.

However, with the recent correction in Sept, the tech sector corrected 10% while MSCI World index only dipped by 4% (as seen in the chart above). This further illustrates the point about diversifying and putting your eggs in the right baskets, at the right time.

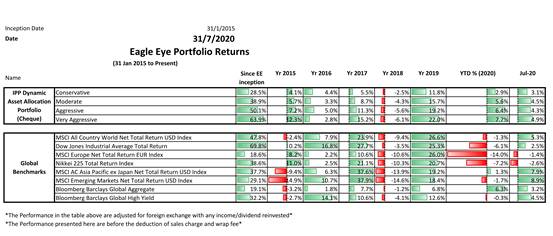

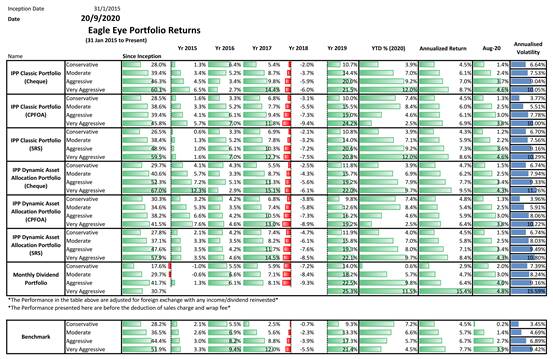

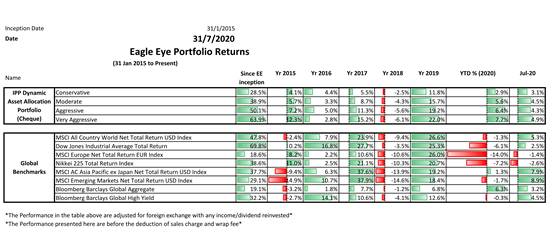

Our IPP Eagle Eye Dynamic Asset Allocation portfolios have delivered stellar returns while managing risks and volatility as we have a dedicated and experienced team managing our portfolios. We have also weathered through the COVID-19 volatility well and even outperformed the MSCI World Index by +9% (as of end July 2020).

2. Stay within your Comfort Zone – Pick the Low-Lying Fruits

Consider starting with a globally diversified ‘bread and butter’ portfolio like the IPP Eagle Eye Dynamic Asset Allocation portfolio or outperforming global funds. Then, slowly add specific themes and sectors once you get more comfortable.

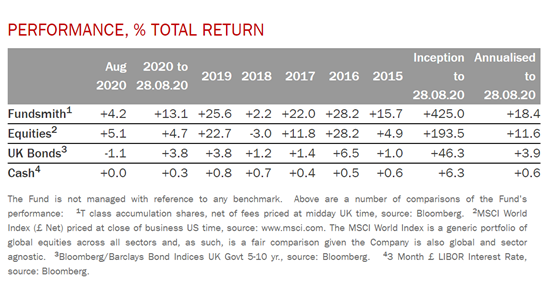

- a. To illustrate the point further, the Fundsmith Equity fund below has produced an annualised return of 18.4% per annum (Total returns of 425%) as of end August 2020 since its inception in November 2010.

- b. Our IPP Eagle Eye Dynamic Asset Allocation (very aggressive) portfolio, has also returned anannualised 9.5% per annum gains since its inception in 2015 (as of 20 Sep 2020). Both offer very decent returns for a bread and butter portfolio and returns have outperformed most major global benchmarks in 2020.

3. Stay Calm Amid Volatility

Many people make losses in the markets because of their emotions. In March 2020 when stocks were tumbling amidst COVID-19 fears, a great number of investors started to panic-sell. However, the market stabilised after a few months, leaving investors with losses that could have been avoided should they have waited it out. On the flipside, those who over-invested during the tech stock boom in the last couple of months would probably have seen their portfolios taking a bigger hit due to the recent market correction in September 2020. Therefore, always keep a clear head during both bearish and bullish markets, and remember to consistently check your greed and insecurities, plan your entrance and exit strategy carefully and rebalance strategically.

Of course, this is often easier said than done. If you have more skin in the game, emotions will amplify exponentially.

To illustrate, if you have $10K in your portfolio vs $1million, a 20% drawdown will feel very different, wealthwise and healthwise. To avoid insomnia or other associated physiological derivatives of market stress during such times, it is best to seek professional management and outsource all the anxiety to your adviser. A good adviser will do his/her best to ensure clients do not make such painful and irreversible emotional mistakes.

“The stock market is a device for transferring money from the impatient to the patient.”

– Warren Buffett.

4. Cut Risk by Aiming for a High Margin of Safety.

Keeping one’s ego in check is important; constantly trying to “beat the market” often results in assuming unnecessary risks and incurring losses. Instead, consider this: Understand the high and low points based on historical data so that you can better determine the margin of safety – a principle of investing where investors purchase securities only when their market price is below their intrinsic prices. Doing this builds a “financial cushion” – giving leeway to better shoulder losses.

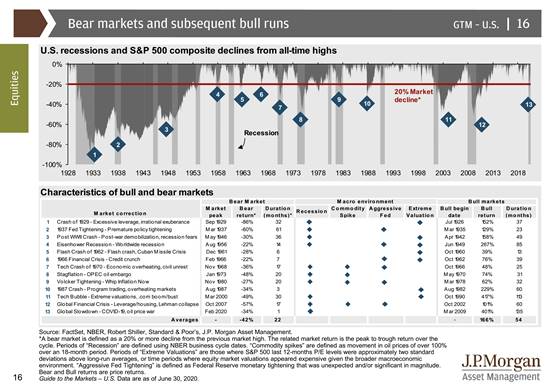

As illustrated above, it is inevitable that markets go into recessions due to its cyclical nature; it is more a matter of when it will happen and how serious the consequent bear market drawdown will be.

From the data above, average Bear market returns in the last 13 Market corrections (including the recent COVID-19 drawdown in March 2020) is -42% whereas average Bull Market returns (excluding the current COVID-19 data since we may not have seen the end of the market recovery) is +166%. This alone illustrates the importance of staying power in the market to increase one’s margin of safety.

Secondly, we made a risk-on call in mid March 2020 to increase our weightage in equities due to the low valuations. From the chart above, -34% drawdown presented a very attractive and high margin of safety point of entry for us. The potential risk to the investor was for the markets to fall further from -34% to the average bear market return of -42%. This presented a potential delta of -8%. Whereas the potential longer term bull market average returns to clients in the illustration above is +166%. With this comfortable margin of safety, we were confident in our call to reap maximum risk-adjusted returns for our clients during the drawdown.

“Confronted with a challenge to distil the secret of sound investment into three words, we venture the motto, ‘margin of safety’,”

– Benjamin Graham, “father of value investing”

5. Complement your Passive Investments with Active Strategic Portfolio Allocations and Rebalancing.

People who invested passively in indices saw their portfolios underperform significantly compared to those who focused on the technology sector during the COVID-19 drawdown. This demonstrates the importance of keeping a close eye on the ever-changing economic and political environment. A lot of holes in the passive investment strategy come clear during crises like this. In this case, the vulnerabilities of certain sectors became a liability to the entire index.

A key and recent case in example was Warren Buffet’s decision to move out of airline stocks, as analysed by CNBC’s Jim Cramer :

“[Buffet]’s perfectly willing to lose money in the short-term if he believes there’s a long-term opportunity, but he didn’t [get aggressive] with the airlines,” Cramer said. “He acknowledged that the facts have changed, and he bailed on the whole group because he knows these stocks are toxic.”

The shutdown of international travel had devastating effects on the airline and tourism sectors and this weighed down greatly on the US indices and consequently dragged down investor’s returns.

Lessons learnt:

a) Keeping a close eye on your portfolios and making strategic adjustments based on changes to the World’s economic and political situations are key to ensuring a robust portfolio and maximising long term total returns.

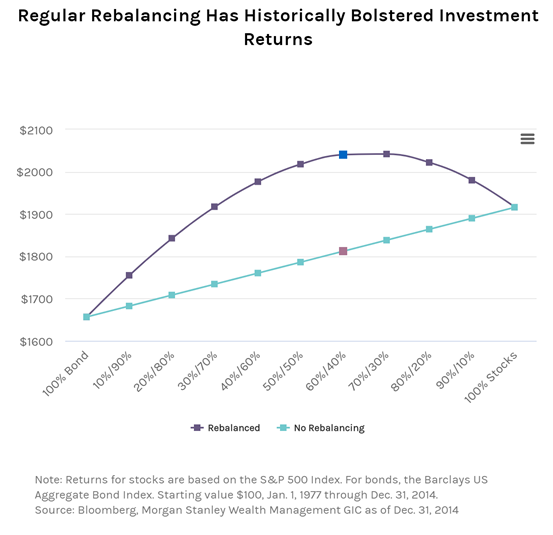

b) Perform active portfolio rebalancing at least once a quarter or half-yearly to ensure you are not over-stretching your risk and taking profits where relevant.

6. Avoid Speculation and Taking Unnecessary Risks.

Consider planning your investment portfolio for the long run if you can. However, if you have to work within a shorter timeframe, de-risk and start diversifying your portfolios gradually into safer instruments such as bonds, retirement products or annuities depending on which best fits your retirement goals. People are often unaware of the options for de-risking their portfolios – if in doubt, always reach out to an experienced adviser to understand your options and help you assess the best fits for your goals.

Catch up with your adviser, or engage one to discuss potential strategies for a resilient portfolio amidst this time of uncertainty today.

| Upcoming Outlook |

| 1. COVID-19 related market volatility There’s been a lot of uncertainties that came along with the pandemic, but the worst is over. Experts have priced in a recovery and we should still expect short-term volatility but that’s not necessarily a bad thing. This is a page from the pandemic playbook – there is a curve, and COVID-19 will ultimately follow the trend. The markets will always work to normalise the pandemic. |

| 2. Robin hood Investing: The High-stakes Trend Robin hood investors and a new breed of investors have mixed things up quite a bit. An example is the car rental company Hertz going bankrupt. Robin hood investors are going in when a traditional investor would steer clear. They add a layer of complexity and unpredictability during this time. Whether or not they have had a major or lasting impact is yet to be seen but it does draw a bit of attention. A good way to deal with this is dollar cost averaging, and picking good baskets to put your eggs in. |

| 3. Surging Gold Prices Gold prices have surged in recent months. Its price has been an interesting development – it is a little pricey right now. Adding gold to one’s portfolio now requires a bit of caution, because one will lose to processing fees. There is a chance that gold will devalue when a vaccine for COVID-19 is found. As of 30 July 2020, gold prices are already destabilising, resulting in a low margin of safety, which means higher risk – hence, caution should be exercised. |

Will/Estate planning services are not provided by IPP Financial Advisers Pte Ltd and is not part of the Financial Advisory Services provided by IPP Financial Advisers Pte Ltd.

Other Adviser Insights

IPP Financial Advisers Pte Ltd

78 Shenton Way #30-01 Singapore 079120 | Tel: +65 6511 8888 | enquiry@ippfa.com | ![]()

![]()

![]()

IPP Financial Advisers Pte Ltd

78 Shenton Way #30-01 Singapore 079120

Tel: +65 6511 8888 | enquiry@ippfa.com

![]()

![]()

![]()